Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership

Page 253 Problem 1 Answer

Given; the exponential depreciation equation

To find: How might a better-fitting exponential depreciation equation look when superimposed over the same scatterplot?

The exponential depreciation function can be determined using exponential regression calculated by hand, by computer software, or by a graphing calculator.

When you use the statistics feature on a graphing calculator, the data is entered into two lists as shown.

The independent variable is the age of the car and the dependent variable is the car value.

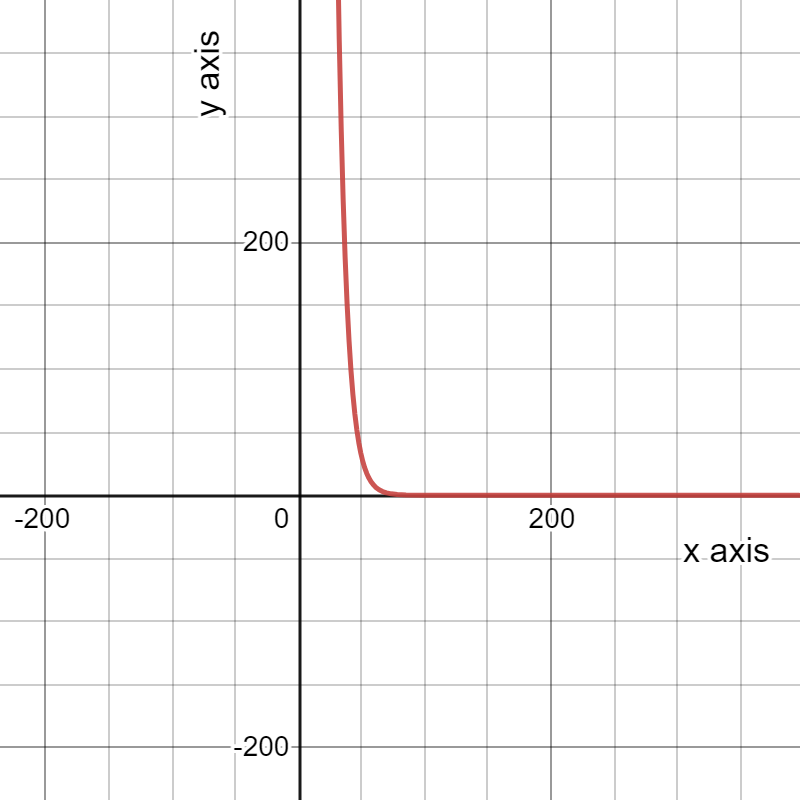

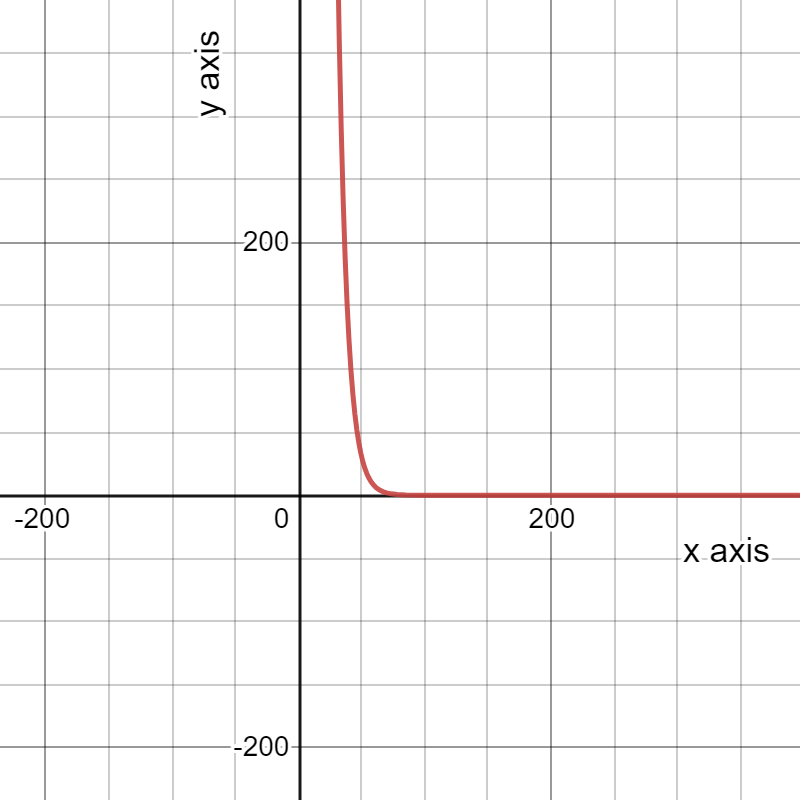

Using the formaty=a×bx,where a=25,921.87 and b=0.92,the exponential depreciation function is y=25,921.87×0.92x.

The graph of this function, superimposed over the scatterplot, appears to be a good fit.

An exponential decay curve fits the following equation: y=e−t/τ.

The graph of the function looks like this

The results become clearer if we take the natural log of both sides:

Hence we conclude that An exponential decay curve fits the following equation: y=e−t/τ.

Read and Learn More Cengage Financial Algebra 1st Edition Answers

The results become clearer if we take the natural log of both sides:

Cengage Financial Algebra Chapter 5.6 Automobile Ownership Guide

Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership Page 254 Problem 2 Answer

Given ; y=a⋆b∧

x,a=32,567.98722,b=0.875378566.

To find: Determine the depreciation percentage.

The exponential decay function was introduced as

y=A(1−r)x.

The graphing calculator uses the format y=a⋅bx.

a=32,567.98722,

b=0.875378566

y=32,567.98722×.87

=28506.75

The depreciation percentage.WILL BE 28.50 %

Hence the depreciation percentage will be given by 28.50 %

Page 255 Problem 3 Answer

Given; A car originally sells for D dollars.

After A years, the value of the car has dropped exponentially to P dollars.

To find: Write an algebraic expression for the exponential depreciation rate expressed as a decimal.

The exponential depreciation equation is of the form y=P(1−r)x with D the original value, P

the depreciation rate per period and A the number of periods.

y=D(1−P%)A

y=D(1−P%)A

Hence an algebraic expression for the exponential depreciation rate expressed as a decimal. y=D(1−P%)A

Solutions For Exercise 5.6 Financial Algebra 1st Edition

Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership Page 256 Problem 4 Answer

Given; value of the car is 22,022. and we have half the purchase so we will divide by 2/11011

A car originally sold for 26,600.a rate of5.5 per year.

To find; How old would the car be had it been purchased at half its value

The length of time, x,

can be determined using the following formula.

x=ln(y/A)

ln(1−r)

Because y equals the value of the car after x years, y = 24,000. The new car price, A, is22,022.

The variable r represents the depreciation rate expressed as a decimal. Therefore, r=0.55

x=ln(22,022/24,000)

ln(1−0.55)

≈0.107

Hence the car was 1 year old approxx , At the time of the purchase, the car was about 0.1077 years old.

Page 257 Problem 5 Answer

Given: I once bought an old car back after I sold it because I missed it so much and I had forgotten that it never ran . . .

I just wanted it back. I could only remember what was good about it. – Connie Chung, Television News Commentator

We have to find that how might the quote apply to what you have learned

Over time, a person could attach an increasing sentimental value to a car and thus the car is then worth more than just some monetary value.

Due to the sentimental value, it might then be difficult to sell a car, because even though the car might not be worth much money, the car might be worth much sentimentally.

We get, Somebody could attach sentimental values to a car

Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership Page 257 Problem 6 Answer

Given: Seamus bought a car that originally sold for $40,000. It exponentially depreciates at a rate of 7.75% per year.

We have to write the exponential depreciation equation for this car.

The exponential depreciation equation is of the form y=P(1−r)x with P the original, r the depreciation rate per period and x the number of periods.

y=40,000(1−0.0775){x}

We get,y=40,000(1−0.0775){x}

Page 257 Problem 7 Answer

Given: Shannon’s new car sold for $28,000. Her online research indicates that the car will depreciate exponentially at a rate of 51/4% per year.

We have to write the exponential depreciation formula for Shannon’s car.

The exponential depreciation equation is of the form y=P(1−r)x with P the original value, r the depreciation rate per period and x the number of periods.

r=51/4%=5.25%=0.0525

y=28,000(1−0.0525){x}

We get, y=28,000(1−0.0525)x

Chapter 5 Exercise 5.6 Automobile Ownership Walkthrough Cengage

Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership Page 257 Problem 8 Answer

Given: Chris purchased a used car for $19,700. The car depreciates exponentially by 10% per year.

We have to find that how much will the car be worth after 6 years?

The exponential depreciation equation is of the form y=P(1−r)x with P the original value, r the depreciation rate per period and x the number of periods.

y=19,700(1−0.10){x}

Replace x with 6

y=19,700(1−0.10)6

=$10,469.39

We get, $10,469.39

Page 257 Problem 9 Answer

Given: y=a⋆bx,a=20,952.11, and b=0.785.

To find: What is the rate of depreciation for this car? How much is this car worth after 6 years, 78 months, and w months?

Exponential depreciation equation: y=P(1−r)x with P as original value, r as depreciation rate and x is the period.

1−b=1−0.785=0.215=21.5%

y=20,952.11×0.7856

=4,902.82

y=20,952.11×0.78578/12

=4,343.91

y=20,952.11×0.785w

Hence, rate of depreciation for this car, car’s worth are respectively: 21.4

%, 4902.82, 4343.91and 20,952.11×0.785w

Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership Page 257 Problem 10 Answer

Given: y=a⋆bx,a=18,547.23, and b=0.8625.

To find: What is the rate of depreciation for this car? How much is this car worth after 6 years, 78 months, and w months?

Exponential depreciation equation: y=P(1−r)x

with P as original value, r as depreciation rate and x is the period.

1−b=1−0.8625=0.1375=13.75%

y=18,547.23×0.86256

=7,635.43

y=18,547.23×0.862578/12

=7,091.09

y=18,547.23×0.8625w/12

Hence, the required results are: 13.75%,$7,635.43,$7,091.09,18,547.23×0.8625w/12

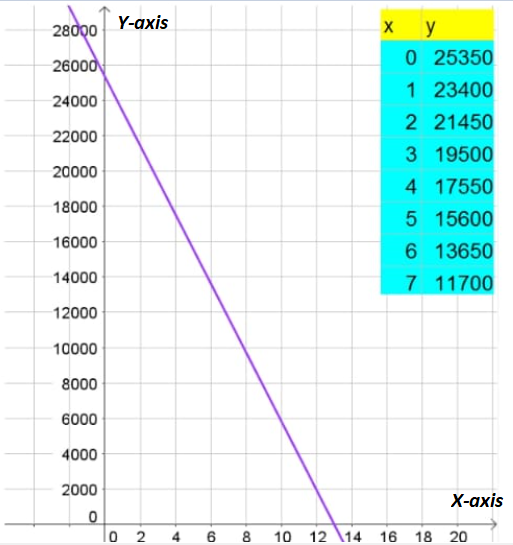

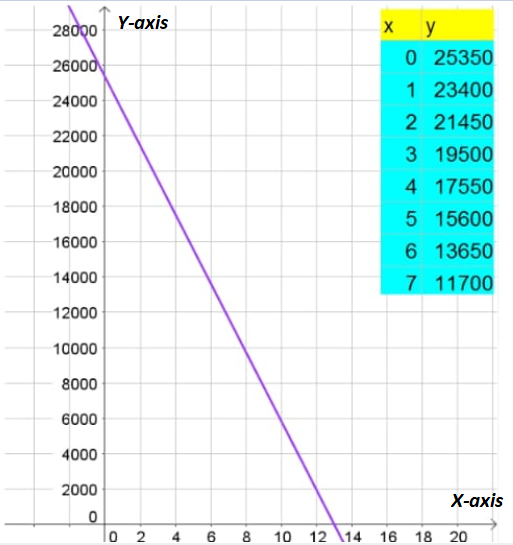

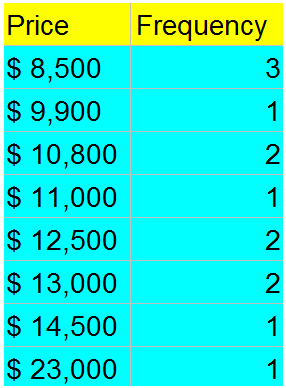

Page 257 Problem 11 Answer

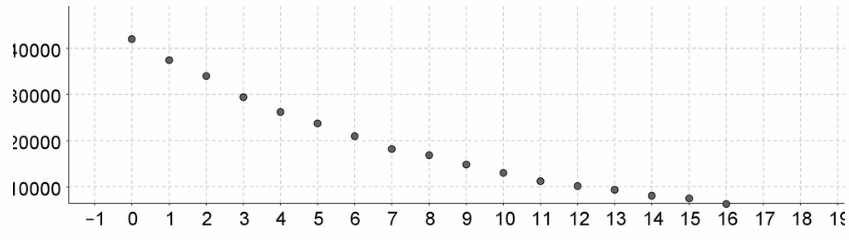

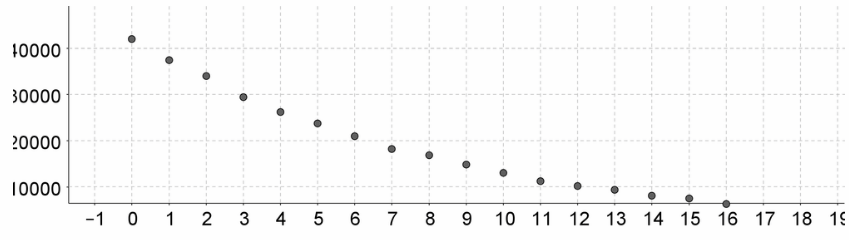

Given: The historical prices of a car are recorded for 17 years as shown.

To find: Construct a scatterplot for the data.

Age is on horizontal axis and value in Dollars on vertical axis:

Hence, the scatter

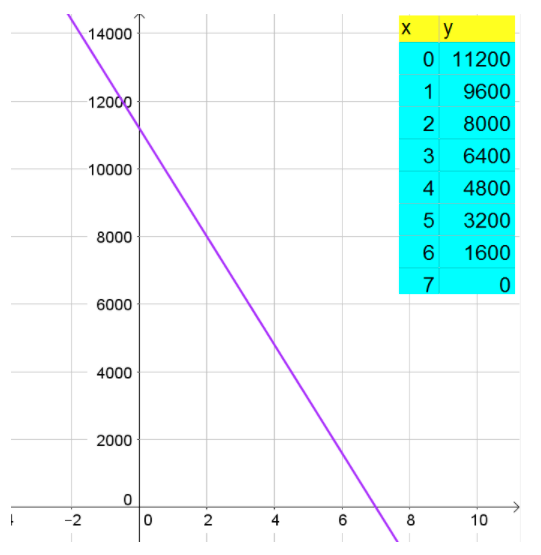

Page 257 Problem 12 Answer

Given: The historical prices of a car are recorded for 17 years as shown.

To find: Determine the exponential depreciation formula that models this data. Round to the nearest hundredth.

Enter the year in list L1 and values in list L2 using the command STAT>1:Edit

Next, we can determine the exponential depreciation using STAT>CALC>0:L1 L2

The calculator then returns:

y=a×bx

a=42,228.36

b=0.89

y=42,228.36×0.89x

Hence, exponential depreciation formula that models this data y=42,228.36×0.89x.

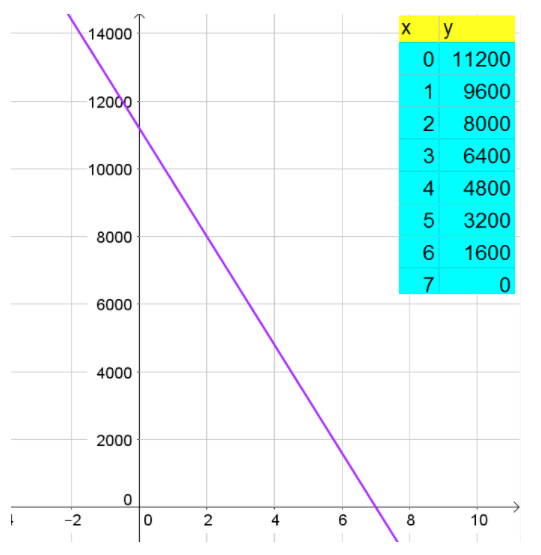

Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership Page 257 Problem 13 Answer

Given: The historical prices of a car are recorded for 17 years as shown.

To find: Determine the depreciation rate.

Since, we have the equation y=a×bx

y=42,228.36×0.89x

And the exponential depreciation equation: y=P(1−r)x

Which implies, 1−r=0.89

r=11

Hence, the depreciation rate is 11%.

Page 258 Problem 14 Answer

Chaz bought a two-year-old car. He paid D dollars. This make and model depreciates at a rate of E percent per year.

Need to write an expression for the original selling price of the car when it was new.

As the exponential depreciation equation is of the form y=P(1−r)x ,where P is the original value,r is the depression rate per period expressed as a decimal and x is the number of periods. We have, y=D

,r=E/100,x=2, Putting the values in the formula gives us:

D=P(1−E/100)2

Further, solving for P gives us:

P=D(1−E/100)2

=D(1−0.01E)2

An expression for the original selling price of the car when it was new is D

(1−E/100)2.

Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership Page 258 Problem 15 Answer

Given a car that originally sells for$30,000 when new but exponentially depreciates after 5 years to $18,700.

Need to tell what is the exponential depreciation rate, expressed as a percent to the nearest tenth of a percent.

As the exponential depreciation equation is of the form y=P(1−r)x,where is the original value,r is the depression rate per period expressed as a decimal and x is the number of periods. We have,P=30,000

,y=18,700,x=5, Putting the values in the formula gives us:

18,700=30,000(1−r)5

⇒0.06233=(1−r)5

⇒0.9098=1−r

Further solving for r gives us:r=1−0.9098

=0.0902

In percentage r=9.02%P

The exponential depreciation rate, expressed as a percent to the nearest tenth of a percent is 9 .02%

Page 258 Problem 16 Answer

Given a car that originally sells for $52,000 when new but exponentially depreciates to$45,000 after 32 months.

What is the exponential depreciation rate, expressed as a percent to the nearest tenth of a percent.

As the exponential depreciation equation is of the form y=P(1−r)x, where P is the original value,r is the depression rate per period expressed as a decimal and x is the number of periods.

We have, P=52,000,y=45,000,x=32/12

When r is the depression rate per year. Putting all the values in the formula gives us:

45,000=52,000(1−r)32/12

⇒0.8654=(1−r)32/12

⇒0.947=1−r

Further solving for r gives us:r=1−0.947

=0.053

In percentage r=5.3%

The exponential depreciation rate per year, expressed as a percent to the nearest tenth of a percent is5.3%.

Cengage Financial Algebra Automobile Ownership Exercise 5.6 Solutions

Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership Page 258 Problem 17 Answer

Given a new car sells for$27,300. It exponentially depreciates at a rate of 6.1% to $22,100.

Need to tell how long did it take for the car to depreciate to this amount and round your answer to the nearest tenth of a year.

As the exponential depreciation equation is of the form y=P(1−r)x, where P is the original value, r is the depression rate per period expressed as a decimal and x is the number of periods.

Using this find the required result.

We have,P=27,300,

y=22,100,

r=0.061,

Putting all the values in the formula gives us:

22,100=27,300(1−0.061)x

⇒0.8095=0.939x

Taking natural logarithm both the sides gives us:

ln0.8095=ln0.939x

Further solving for x

gives us:x=ln0.8095

ln 0.939

=3.4

Rounding your answer to the nearest tenth of a year, it take3.4 years for the car to depreciate to this amount.

Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership Page 258 Problem 18 Answer

Given Amber bought a used car valued at $16,000. When this car was new, it was sold for$28,000.

If the car depreciates exponentially at a rate of 9% per year, then approximately how old is the car.

As the exponential depreciation equation is of the form y=P(1−r)x, where P is the original value,r is the depression rate per period expressed as a decimal and x is the number of periods.

Using the given formula, find the required result.

We have,P=28,000,

y=16,000,

r=0.09

Then, putting the values in the formula gives us:

16,000=28,000(1−0.09)x

⇒0.5714=0.91x

Taking natural logarithm both the sides gives us:

ln0.5714=ln0.91x

⇒ln0.5714=xln0.91

Solving for x gives us:

x=ln0.5714

ln0.91

=5.9

If the car depreciates exponentially at a rate of 9%per year, then the car is approximately 5.9 years old.

Cengage Financial Algebra 1st Edition Chapter 5 Exercise 5.6 Automobile Ownership Page 258 Problem 19 Answer

Given a car originally sold for$25,900. It depreciates exponentially at a rate of 8.2% per year.

Nina put$10,000 down and pays $550 per month to pay off the balance.

Need to tell after how many years will her car value equal the amount she paid for the car to that point and what will that value be.

As the exponential depreciation equation is of the form y=A(1−r)x, where A is the original value of the car,r is the depression rate per period expressed as a decimal and x is the number of periods and y is the value of the car after x years.

Using this formula, find the required result.

We have,A=25,900,

r=0.082,

In one year,y=10,000+550(12x),

Putting the values in the formula gives us:

10,000+550(12x)=25,900(1−0.082)x

⇒10,000+6,600x=25,900(0.918)x

Solving for x using a calculator gives us x=1.83804.

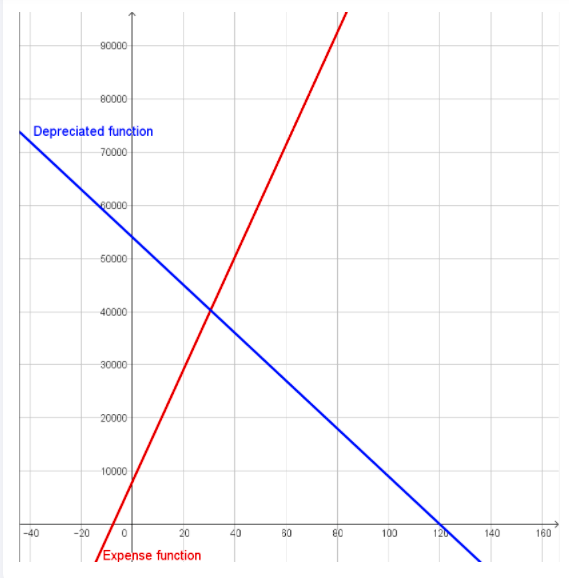

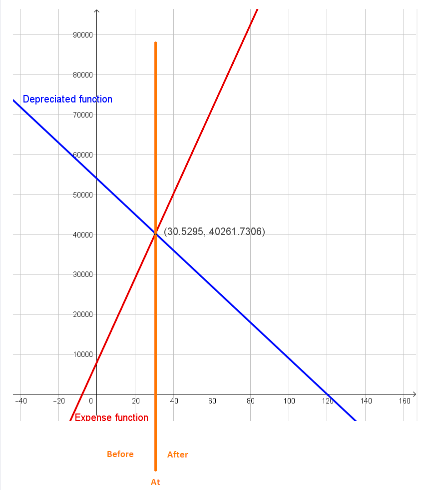

Substitute the valus of x in y,

Then,y=$10,000+$550(12×1.83804)

=$22,131.11

Rounding the value gives usy=$22,131.

After 1.83804 years her car value equal the amount she paid for the car to that point and the value will be$22,131 (rounded).

How To Solve Cengage Financial Algebra Chapter 5.6 Automobile Ownership

Page 258 Problem 20 Answer

Given Jazmine’s car originally sold for $46,000.It depreciates exponentially at a rate of 10.3%per year.

Jazmine put$12,000 down and pays $800 per month to pay off the balance.

Need to tell after how many years will her car value equal the amount she paid to date for the car and what will that value be.

The exponential depreciation equation is of the form y=A(1−r)x, where A is the original value,r is the depression rate per period expressed as a decimal and x is the number of periods and y is the value of the car after x years.

Using this find the required result

We have,A=46,000,

r=0.103,

In one year,y=12,000+800(12x),

Putting the values in the formula gives us:

12,000+800(12x)=46,600(1−0.103)x

⇒12,000+9,600x=46,600(1−0.103)x

Solving for x

using a calculator gives us x=2.46372.

Substitute the value of x in y:

Then,y=$12,000+$800(12×2.46372)

=$35,651.71

≈$35,652

After 2.46372 years her car value equal the amount she paid for the car to that point and the value will be $35,652 (rounded).